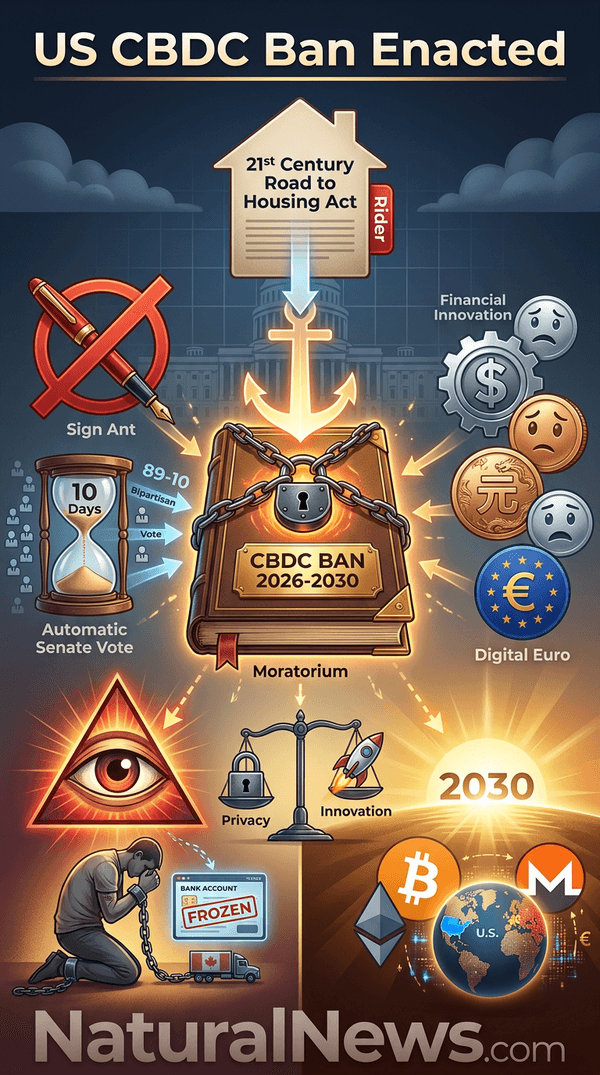

A ban on the Federal Reserve issuing a central bank digital currency (CBDC) directly to individuals is set to take effect after being attached to a housing bill that became law without President Donald Trump’s signature, according to the bill text and officials. The measure, part of the 21st Century Road to Housing Act, prohibits the Fed from creating a retail CBDC until at least 2030, according to the legislation. The housing bill, which also includes provisions for affordable housing funding, passed Congress with bipartisan support and became law after a 10-day period during which Trump neither signed nor vetoed it, officials said.

Under the Constitution, a bill presented to the president that is not signed or vetoed within 10 days while Congress is in session automatically becomes law, according to officials. The CBDC ban was included as a rider in the broader legislation. The Senate passed the bill with an 89-10 vote in March 2026, according to reports [8].

Legislative Path and Trump’s Inaction

The CBDC ban was inserted as a rider into the 21st Century Road to Housing Act, a sweeping bipartisan bill aimed at addressing housing affordability, according to congressional records. Trump had long opposed central bank digital currencies. During a speech at the Bitcoin Conference 2024 in Nashville, Trump stated, “There will never be a CBDC while I am president” [2]. In January 2025, he signed an executive order explicitly banning federal agencies from establishing or promoting CBDCs [1].

Despite those actions, Trump on June 24, 2026, canceled a planned Capitol Hill signing ceremony for the housing bill, demanding that Congress first pass the SAVE America Act, an elections measure he had elevated as a top legislative priority [7]. The bill had already passed the House and Senate, and because Trump did not return it with a veto within the 10-day period while Congress remained in session, it became law without his signature, according to government procedure.

Supporters and Opponents Weigh In

Proponents of the ban, including privacy advocates and some Republican lawmakers, argue that a retail CBDC would enable excessive government surveillance and control over personal finances. A Liberty Counsel analysis warned that such a currency could be used to “spy on you and exert ultimate control over your freedom” [9]. Firo co-founder Reuben Yap has said that CBDCs give central banks “a lot of fine-grained control over how you should be spending your money” [3]. Privacy advocates have cautioned that these systems could lead to a “digital prison” where convenience comes at the cost of freedom, as noted in a Trends Journal analysis [4].

Opponents, including some financial technology groups and Democratic lawmakers, claim the ban stifles innovation and leaves the United States behind other nations that are developing CBDCs. The Digital Dollar Project stated in a release that “a flat prohibition prevents the US from exploring potential benefits like faster payments and financial inclusion.” Meanwhile, other countries are moving ahead: China has rolled out a digital yuan, and the European Parliament in July 2026 voted to back a digital euro [5][6].

Implications and Next Steps

The Federal Reserve has stated it will comply with the law, ending its previous research into a retail CBDC, according to a Fed spokesperson. The ban does not affect wholesale CBDCs—used for interbank settlements—or private stablecoins, the bill clarifies. Observers have noted that the law could face legal challenges, but no lawsuits had been filed as of press time, officials said.

The housing bill’s other provisions, including funding for affordable housing projects, are already being implemented, according to officials. The ban represents a significant legislative check on executive branch efforts to introduce a digital dollar, though the debate over digital currencies is likely to continue as technology evolves and other nations advance their own CBDC initiatives.

References

- Ramon Tomey. "CBDCs officially BANNED under new Trump executive order, fulfilling his campaign promise". NaturalNews.com. January 25, 2025.

- NaturalNews.com. "Trump vows to BAN central bank digital currencies There will never be a CBDC while I am president". July 31, 2024.

- NaturalNews.com. "Reuben Yap: CBDCs let central banks CONTROL how people spend their money". August 10, 2023.

- Trends-Journal-2022-11-34.

- Trends-Journal-2021-10-29.

- "EU Parliament Votes to Back Digital Euro". July 10, 2026.

- "Trump Cancels Housing Bill Signing That Would Ban CBDCs - Demands Action On SAVE Act First". June 24, 2026.

- Vince Quill. "US Senate Votes To Include CBDC Ban In Bipartisan Housing Bill". March 13, 2026.

- Liberty Counsel. "Senate legislation would allow dangerous central bank digital currencies after 2030". June 1, 2026.

Explainer Infographic

Please contact us for more information.