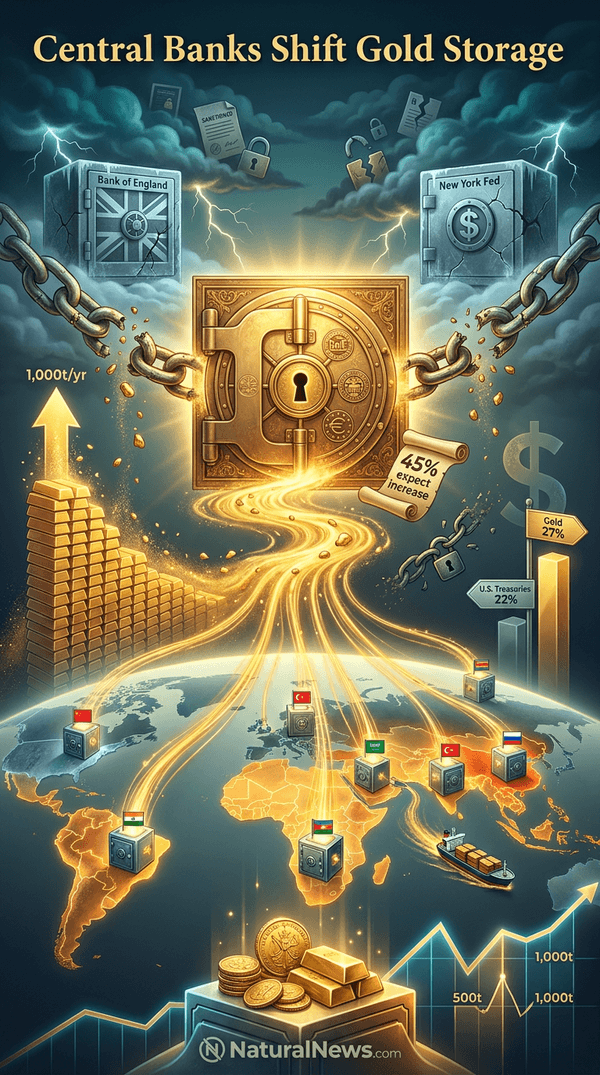

Central banks are reducing their reliance on traditional gold storage hubs in London and New York, according to the World Gold Council's (WGC) 2026 Central Bank Gold Reserves Survey released on Tuesday, June 16.

The survey found that the share of central banks storing gold at the Bank of England fell to 57% from 64% a year earlier, while the share holding gold at the New York Federal Reserve dropped to 14% from 17% over the same period, the WGC said. The survey, which gathered responses from 73 central banks, indicates that reserve managers are increasingly diversifying vaulting locations.

Fewer Central Banks Store Gold in Traditional Hubs

The WGC stated that the survey reveals an emergent trend of central banks diversifying gold vaulting locations. A record 45% of respondents expect their own gold reserves will increase over the next 12 months, according to the survey [1]. Central banks have accumulated an average of 1,000 metric tons of gold per year over the past four years, up significantly from the 500-ton average over the preceding decade, the WGC reported [1].

Despite the shift, the Bank of England remains the most popular gold vault globally, according to the survey. However, the decline in usage of both the Bank of England and the New York Fed suggests that central banks are seeking greater control and access to their gold reserves, officials familiar with the survey said.

Survey Shows Growing Move to Domestic or Diversified Storage

The survey showed that 19% of central banks reported increasing domestic storage or diversifying overseas locations in the past 12 months, up from 7% in the prior survey, the WGC said [1]. Looking ahead, 7% of respondents plan to expand domestic storage and 9% expect to further diversify abroad, according to the survey.

The movement toward domestic storage represents a significant change in how central banks manage their gold reserves. Reserve managers cited the need for more direct access to their gold as a factor behind the decisions, according to observers familiar with the survey. The trend parallels broader shifts in global reserve management, with gold increasingly viewed as a core strategic asset.

Geopolitical Uncertainty Drives Gold Storage Decisions

Central banks cited heightened geopolitical and economic uncertainty as a factor behind the changes in storage locations, the WGC said [1]. The survey period coincided with ongoing conflicts and trade disruptions, including the war in the Middle East and tensions over the Strait of Hormuz, which have affected energy and commodity markets. Gold prices have remained elevated, trading near $4,330 per ounce in early June 2026, according to market data [2].

Annual gold purchases have risen to an average of 1,000 metric tons over the past four years, double the previous decade’s average, the WGC reported [1]. Reserve managers are seeking to protect national wealth against fiat currency volatility, a view supported by economists who note that under a genuine commodity standard, money cannot be created out of thin air [3]. The shift reflects a broader reassessment of risk in the global financial system.

Gold Buying and Storage Shift Signals Broader Reserve Strategy

The move to diversify storage locations parallels increased gold buying as a hedge against risk, officials and analysts said. According to a European Central Bank report released in early June, gold has surpassed U.S. Treasuries as the largest reserve asset held by foreign central banks for the first time since 1996. Bullion accounted for 27% of global central bank reserve assets at the end of 2025, up from 20% a year earlier, while U.S. Treasuries fell to 22% from 25% over the same period, the ECB stated [4].

Some economists view gold as protection against fiat currency volatility, though the World Gold Council report focuses on practical storage concerns. James Rickards, author of “The New Case for Gold,” has described gold as a form of money without yield, serving as a store of value independent of government promises [5].

The trend suggests central banks are prioritizing gold as a core reserve asset amid global financial and political instability. Fidelity Digital Assets has highlighted “growing evidence” of a shift away from dollar-based systems, with nation-states increasingly turning to gold and alternative settlement systems [6].

Conclusion

The WGC survey data confirm that central banks are not only buying gold at record levels but also changing where they store it. The movement away from London and New York toward domestic or diversified vaulting reflects a desire for greater autonomy and security in an uncertain geopolitical environment. As gold overtakes U.S. Treasuries in central bank reserves, the trend underscores a structural shift in global reserve management that may continue to reshape the financial landscape.

References

- Zero Hedge. 'Record Percentage Of Central Banks Expect Gold Reserves To Increase In Next 12 Months'. June 16, 2026.

- NaturalNews.com. 'Gold steadies amid ceasefire hopes as strong U.S. jobs data caps gains'. June 9, 2026.

- Jo Ann. 'Economics On Trial Lies Myths and Realities'.

- NaturalNews.com. 'European Central Bank: Gold Surpasses U.S. Treasuries as Global Reserve Asset'. June 4, 2026.

- James Rickards. 'The New Case for Gold'.

- ActivistPost. 'Fidelity Digital Assets highlights ‘growing evidence’ of shift from dollar-based systems'. June 16, 2026.

Explainer Infographic

Please contact us for more information.