Wells Fargo abruptly ended its business with a well-known gun dealer in a move emblematic of the increasing hostility big banks are showing towards the firearms industry.

(Article by Stephen Gutowski republished from TheReload.com)

With little explanation, the bank closed the business and personal accounts of Brandon Wexler just before Christmas. After 25 years with a personal account and 14 years with a business account, Wexler was given about a month to find a new bank. As owner of Wex Gunworks in Delray Beach, Florida, Wexler has been cited in countless major media reports for years, but Wells Fargo said his business had suddenly become too risky.

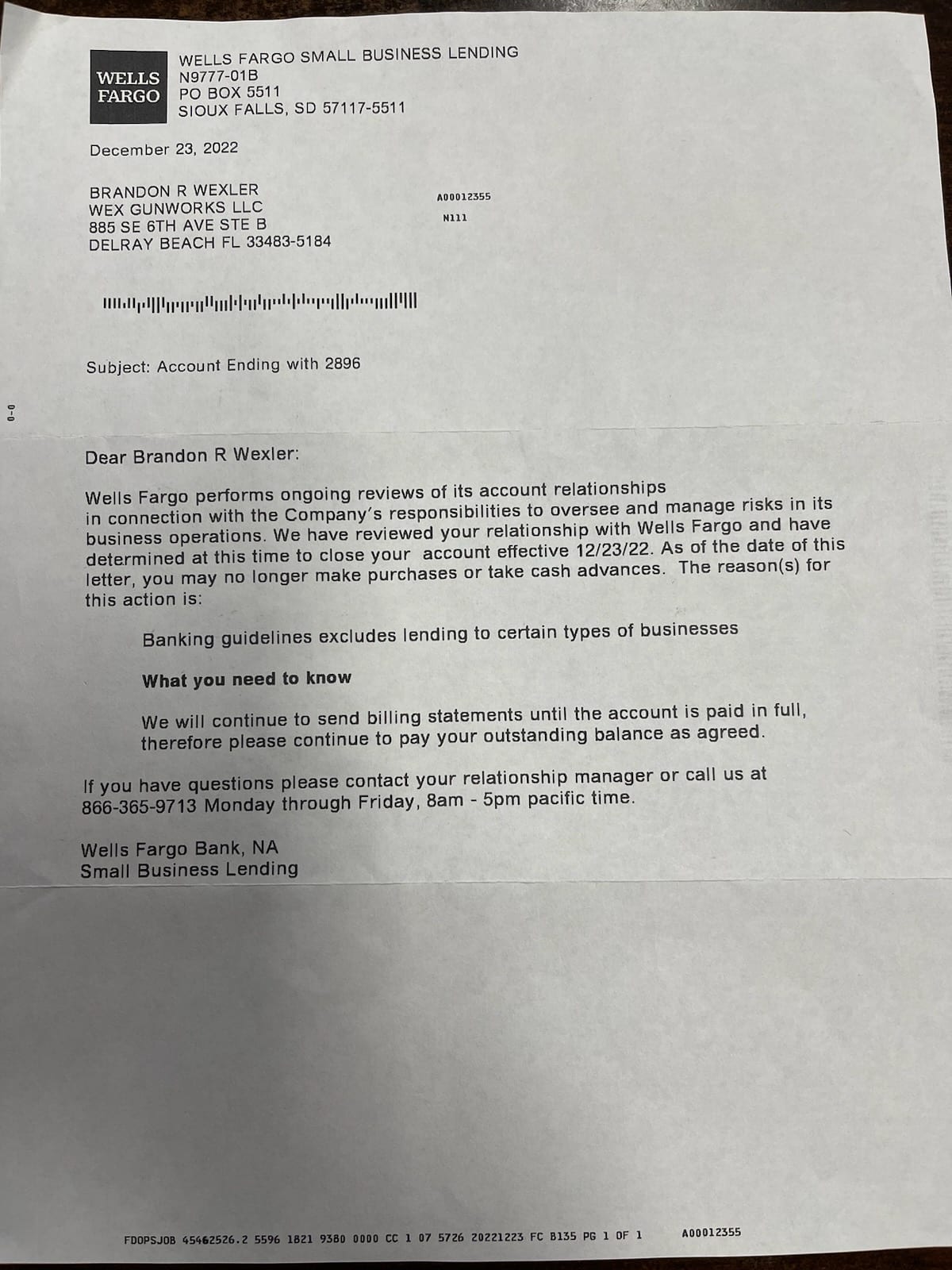

“Wells Fargo performs ongoing reviews of its account relationships in connection with the Bank’s responsibilities to manage risks in its banking operations,” the bank said in a December 22nd letter to Wexler. “We recently reviewed your account relationship and, as a result of this review, we will be closing your above-referenced accounts.”

Another letter sent the following day informing Wexler that Wells Fargo was canceling his business line of credit said, “the reason(s) for this action is: Banking guidelines excludes lending to certain types of businesses.” But the letters offered no further details, and Wexler said none of the officials at his local branch offered any either.

“I’ve been with them for 25 years,” he told The Reload. “I’m a professional fireman. I do everything the right way. It’s messed up.”

Wexler, who has been cited in stories by the New York Times, Washington Free Beacon, CNN, ABC, and many more publications, said nothing had changed with his business. He said he believed the move by Wells Fargo was motivated entirely by animus against the gun industry.

We are building the infrastructure of human freedom and empowering people to be informed, healthy and aware. Explore our decentralized, peer-to-peer, uncensorable Brighteon.io free speech platform here. Learn about our free, downloadable generative AI tools at Brighteon.AI. Every purchase at HealthRangerStore.com helps fund our efforts to build and share more tools for empowering humanity with knowledge and abundance.

“It feels like it’s a direct attack against gun dealers,” he said. “This all just happened recently, and we have been in business for many years. I’ve never ever seen anything like this.”

Jennifer L. Langan, Head of communications for CSBB & Consumer Lending at Wells Fargo, disputed Wexler’s claim that the closures were due to his work as a gun dealer.

“Based on our analysis of the risk associated with this customer, we made a decision to close the accounts,” she told The Reload. “Our decision is not based on the industry.”

She said she could not disclose the details behind the decision, but reiterated that Wells Fargo has never announced a policy against doing business with gun companies.

The National Shooting Sports Foundation (NSSF), which represents gun makers and dealers, said what happened to Wexler is part of a growing trend.

“Wells Fargo’s decision to abruptly cancel all business ties with Wex Gunworks is the most recent example of “woke” banking discrimination against the firearm industry,” Mark Oliva, an NSSF spokesman, told The Reload.

The nation’s largest banks have been actively cutting ties with gun makers and dealers for years in an attempt to force the industry to stop selling firearms, such as the popular AR-15, that executives disapprove of Americans owning. The effort was initiated as part of an Obama Administration program known as Operation Chokepoint, where regulators pressured financial institutions not to do business with disfavored industries, including the firearms industry. After the program was exposed and discontinued, behemoths like Citibank and Bank of America still enacted policies against working with companies that make or sell certain guns or ammunition.

Wells Fargo was initially a notable exception to the trend among major banking conglomerates. It resisted efforts by activist investors to cancel business the bank did with top American gun maker Ruger. It never publicly announced a policy against working with gun businesses as other big banks have done.

However, Wells Fargo has begun signaling a shift against guns in recent years. In 2019, it committed to donating $10 million to “gun violence research.” A year later, it said it planned to cut ties with the National Rifle Association.

Now, it may be starting to quietly cut decades-long ties with small gun dealers like Wexler. While they may be able to find other banks to work with, being shut out of doing business with major financial institutions limits their options for growth or even survival.

Oliva said the gun industry is trying to counter the efforts of banks like Wells Fargo through new legislative measures.

“NSSF has been battling this “woke” banking discrimination by working with state legislatures to introduce and enact the Firearm Industry Nondiscrimination (FIND) Act, similar to the law that was passed last year in Texas,” he said. “That law states that if banks cannot certify that they do not hold discriminatory policies of refusing business to firearm businesses simply for being “in the business,” they forfeit their opportunity to compete for state and municipal contracts.”

NSSF is currently waiting on Texas Attorney General Ken Paxton (R.) to decide if Citi and JP Morgan are violating the law despite the banks claiming they don’t discriminate against gun companies. Oliva said Oklahoma has already introduced a version of the FIND act, and NSSF expects more states to do so in short order.

“Taxpayers should not be forced to fund gun control forced through nameless and faceless corporate boardrooms that exceeds federal and state law,” he said.

Florida doesn’t have a similar policy in place. So, Wexler’s options are likely pretty limited. He said he is exploring whether he has a legal case against Wells Fargo, though.

“I don’t care about the money,” he said. “It’s more about making a point here.”

At the very least, Wexler said he wants to raise awareness of what happened.

“The public really needs to know about this,” he said. “It’s not right.”

UPDATE 1-12-2023 3:42 PM EASTERN: This piece has been updated with additional comments from Wells Fargo.

Read more at: TheReload.com

{kind=link}

{kind=link}

Please contact us for more information.